The Original Sin

How The Hundred Became English Cricket's Greatest Sleight of Hand

By Gary Mason & Simon Aldis

This isn’t an opinion piece. It’s a forensic trail through the ECB’s own numbers. The figures published in its audited accounts across the decade from 2015 to 2025. Within those filings, the ECB sets out its reserve policy and repeatedly notes that its financial buffer sits below the level it considers desirable.

What the ECB has not set out in plain language is what that pressure meant for strategic decision-making and whether the creation of The Hundred should be read not only as an audience-growth project, but also as a financial stabilisation strategy.

A note on the figures: The ECB reports at two levels:

· The ECB company (the parent entity), the legal body that contracts, distributes, and carries key liabilities.

· The ECB group, the consolidated position, combining the parent with subsidiaries, including the England and Wales Cricket Trust and other entities within the reporting perimeter.

Company figures reflect the parent entity’s own balance sheet, where the decisions are made and the liabilities sit. Group figures consolidate subsidiaries, including the England and Wales Cricket Trust, a registered charity whose funds cannot be used for ECB operations. That distinction matters when assessing the ECB’s financial health.

Unless stated otherwise, this article uses ECB company figures. Where group figures are used, this is noted.

Every responsible organisation holds a financial buffer. The ECB is no different. In a statement cited in parliamentary evidence, the ECB has said its reserves exist to protect the organisation from the unexpected cancellation of a major international series, the kind of disruption that can remove a large chunk of expected income in a single season.

Its audited accounts describe a desired reserve level of 40% of turnover. The same accounts confirmed, repeatedly, that the ECB was falling short of it.

This is not a technical detail. Once a governing body publishes a reserve policy, it becomes a test of stewardship, did management run the sport with adequate self-insurance, or did it allow the buffer to collapse and then need a high-stakes strategy to rebuild it.

The financial pressures on the ECB have been reported before. George Dobell at The Cricketer and others have written about the state of the ECB’s reserves and the strain of county distributions. The parliamentary evidence cited in this article is a matter of public record. None of this is hidden.

What has not been drawn together, as far as we are aware, is the full timeline: the reserves trajectory mapped against each strategic decision in the creation and sale of The Hundred, using the ECB’s own published figures across a decade of audited accounts.

What the Numbers Show

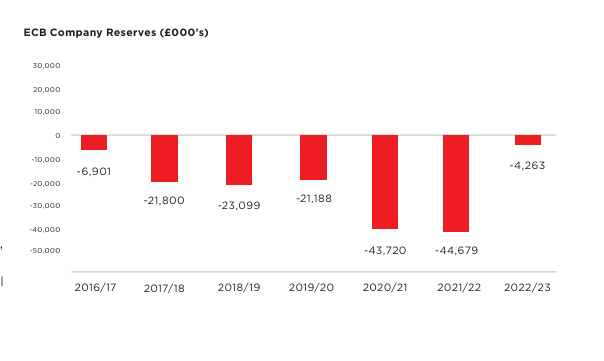

Year ended 31 January 2016, the ECB company’s reserves were +£22.910m.

Year ended 31 January 2017: -£6.9m (now negative)

Year ended 31 January 2018: -£21.8m

Year ended 31 January 2019: -£23.1m

Year ended 31 January 2020: -£21.2m

Written evidence submitted to Parliament was blunt about what had happened. The distributions made to counties in the year ending January 2018 were, it noted, ‘money that the ECB had largely not earned.’ Over four years, distributions had exceeded earnings, producing cumulative losses of £61.3 million.

The same evidence observed that the ECB had previously said its reserves existed to protect the organisation from the unexpected cancellation of an ODI series or a pair of back-to-back Tests. With reserves now depleted, the submission warned, ‘risks from unexpected events can have severe consequences.’ That warning was written before anyone had heard of Covid-19.

This was not a slow bleed caused by external forces. The ECB’s own 2017/18 accounts acknowledged that reserves had fallen “at a faster rate than originally modelled” because special fee distributions had been made to the county network ahead of schedule.

In the same report, the ECB states that equity reserves in the short term are scheduled to remain below its desired benchmark of 40% of turnover, albeit partly offset by significant cash holdings through the period.

By the year ended 31 January 2021, the ECB’s own “ECB Company Reserves (£000s)” chart shows company reserves of -£43.720m.

Source: ECB Company Reserves chart, ECB Financial Statements 2022/2023, Strategic Report (p.4). Company reserves stood at +£22.9m the year before this chart begins. Audited by KPMG.

At group level, the consolidated balance sheet shows members’ funds of £2.2m.

In its Strategic Report for that year, the ECB states that the fall in revenue and profit “reflects the significant impact that COVID-19 has had on ECB’s finances due largely to the postponement of ECB’s new competition, The Hundred, until 2021, alongside the additional costs of operating bio-secure international cricket.

The Timeline

Now place the ECB’s strategic decisions against that financial trajectory.

September 2016: the counties informally vote 16–3 in favour of developing a new city-based competition.

The formal vote to amend the ECB’s Articles of Association follows on 26 April 2017, passing 38–3.

ECB company reserves, which stood at +£22.9 million at the start of the 2016/17 financial year, would be -£6.9 million by the end of it.

October 2017: the 100-ball format is first proposed by the ECB’s chief commercial officer during a scouting trip to a resort in Spain. Company reserves are already -£6.9 million and falling.

Also in 2017, the ECB secures a £1.1 billion broadcast deal for 2020–2024, the largest in the ECB’s history, with The Hundred as its flagship new product.

April 2018: The Hundred is publicly announced. Company reserves stand at -£21.8 million.

The Hundred finally launches in the summer of 2021. At the end of January that year, company reserves stood at -£43.7 million.

What Already Existed

The ECB already had a short-format competition. The T20 Blast ran across all 18 counties with established local rivalries and growing crowds. By 2019, average Blast attendances had risen 47% in five years.

Surrey were regularly selling out at The Oval. Somerset were sold out. Sussex sold out six of their seven home matches.

It was a competition rooted in the existing structure of English cricket, and it was working.

The ECB chose to build something new rather than back what was already working. It created eight city-based franchises in a format played nowhere else in world cricket, designed from the outset for broadcast value.

The teams were incorporated as separate companies in May 2019, more than two years before the first ball was bowled.

The ECB’s own 2020 accounts state: “During 2019 the ECB became a shareholder of the eight Hundred Team companies, the companies are private companies limited by shares, which were incorporated on 10 May 2019.”

The Public Narrative

The Hundred was presented to the public as a growth strategy. The ECB spoke of attracting new audiences, of “mums and kids,” of simplifying the game for people who didn’t follow cricket. Mumsnet was consulted. Andrew Strauss, then director of England cricket, talked about reaching “a different audience.” The message was consistent: this was about expanding the game.

The financial statements tell a different story. Every key decision in the creation of ‘The Hundred’ was made during a period when the ECB company’s reserves were falling, negative, or both. The product that emerged was perfectly shaped to anchor a major broadcast deal and generate the revenue needed to stabilise the balance sheet. The ECB’s most recent accounts explicitly include the sale of Hundred franchise stakes in their financial forecasts.

The Question

This article makes no claim about what was said in ECB boardrooms. It doesn’t need to. The published accounts speak loudly enough.

A national governing body’s reserves went negative and stayed negative for five consecutive years. By 2021, the company was £43.7 million underwater. During that exact period, the same body designed a brand-new competition, not to replace what wasn’t working, but to replace a T20 Blast that was breaking attendance records.

It optimised that competition for broadcast value. It incorporated the teams as separate companies more than two years before the first ball was bowled.

It secured a £1.1 billion broadcast deal with The Hundred as its flagship new product. It then sold the franchise stakes to private investors, including IPL ownership groups, for over £500 million.

Counties across the network remain financially fragile. Sussex entered ECB special measures in 2026. The Blast has been cut back.

The domestic calendar has been bent around a franchise product built on a format nobody else in world cricket has adopted. The Hundred format that the ECB’s own chief executive has publicly said he is open to scrapping in favour of T20.

Every step of this sequence is documented in the ECB’s own published accounts and public statements. No leaked emails. No unnamed sources. Just the numbers, published by the ECB, audited by KPMG, and available to anyone who cares to read them.

The only question is whether the ECB built The Hundred to grow English cricket, or to dig itself out of a financial hole of its own making. The accounts don’t answer that question. But they make it very hard to avoid asking it.

Before the sale, every pound of Hundred revenue stayed inside the game’s ecosystem. Now, private investors hold equity stakes that entitle them to a share of the profits generated by English cricket’s broadcast deals. That value leaves the game. It does not come back.

When you sell control of the game to private investors, you don’t just lose control of the money. You lose control of who plays.

All financial figures cited are drawn from the ECB’s published audited accounts and written evidence submitted to Parliament. Company figures refer to England and Wales Cricket Board Limited. Group figures refer to the consolidated group including the England and Wales Cricket Trust.

Sources

ECB Annual Report & Consolidated Financial Statements, Year Ended 31 January 2020

ECB Financial Statements 2020/2021

ECB Financial Statements 2017/2018

ECB Group Annual Accounts 2024/2025

Written evidence CRI0005, submitted to the Parliamentary inquiry into the future of English cricket

Written evidence submitted by Oppose The Hundred to Parliament

ESPNcricinfo, “’It’s still up for grabs,’ say counties, despite city cricket vote” — http://www.espncricinfo.com/story/_/id/17561126/-grabs,-say-counties,-city-cricket-vote

Sky Sports, “City-based Twenty20 competition approved for 2020 by ECB vote” https://www.skysports.com/cricket/news/12123/10851616/city-based-twenty20-competition-approved-for-2020-by-ecb-vote

Open To Discussions On Changing The Hundred Format To T20, Says ECB CEO | England Cricket News Today

CRICKET FILES - LEGAL NOTICE.

Cricket Files is an independent investigative journalism and commentary series produced by Gary Mason and Simon Aldis. The content published under the Cricket Files name, including video, written articles, and social media posts, constitutes journalism, analysis, and opinion on matters of public interest.

Honest Opinion (Section 3, Defamation Act 2013): Where Cricket Files content expresses views, conclusions, or commentary, these constitute honestly held opinions based on facts that are stated, referenced, or otherwise available at the time of publication.

Publication on a Matter of Public Interest (Section 4, Defamation Act 2013): The producers reasonably believe that publication of this content is in the public interest.

Truth (Section 2, Defamation Act 2013): Where Cricket Files content states facts, those facts are believed to be substantially true and are based on publicly available records, official publications, court documents, and/or information provided by sources whose reliability has been assessed in good faith.

Right of Reply: Cricket Files operates a standing policy of offering a right of reply to any individual or organisation that is the subject of its reporting.

Copyright: All Cricket Files content is © Gary Mason and Simon Aldis. All rights reserved.

Good detail and an interesting read, but I think it has been clear for some time that the Hundred was created as piece of ECB IP that could be sold. The ECB didn’t have the right to sell the Blast, hence the need to create an alternative. On that one measure (motivation aside) it has been very successful. IP created, large sale of IP achieved in a short space of time. Excellent for the balance sheet of all concerned in the short term. We shall now watch the consequences (for there will be consequences, there is no free lunch) unfold over the next few years.